Which States Have No Lottery Tax?

By Wade Coltson · April 16, 2026 · 5 min read

Where you live when you win the lottery is one of the most significant factors in how much you actually keep. Federal taxes apply equally to all winners across the country, but state income taxes vary dramatically. On a large jackpot, the difference between living in a high-tax state versus a no-tax state can easily exceed $30 to $50 million.

Seven states currently do not impose a state income tax on lottery winnings. Understanding why they do not, and what that means in real dollar terms, helps frame just how much location affects the math.

The No-Tax States

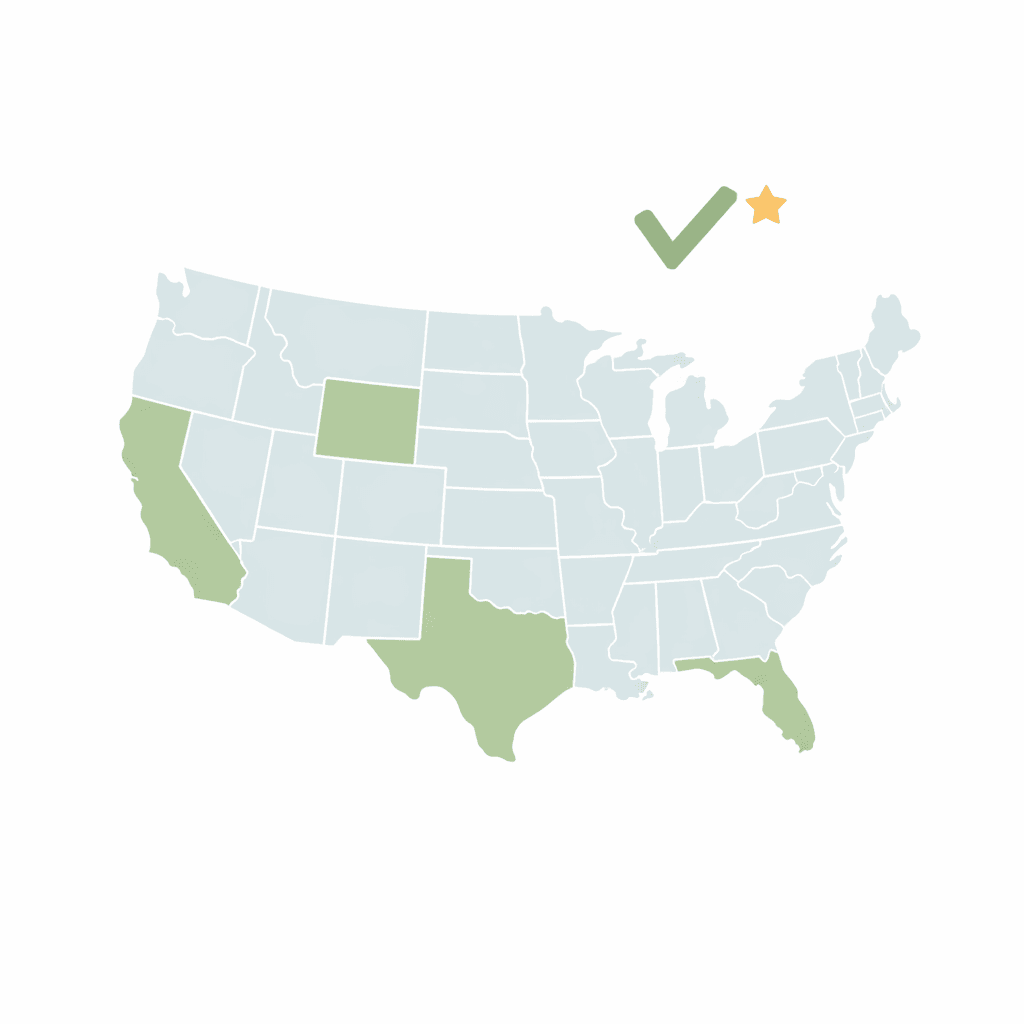

The following states do not tax lottery prizes at the state level. Winners in these states owe federal income taxes but nothing additional to the state.

- Florida — No state income tax of any kind

- Texas — No state income tax of any kind

- Washington — No state income tax of any kind

- Wyoming — No state income tax of any kind

- South Dakota — No state income tax of any kind

- Tennessee — No state income tax of any kind

- New Hampshire — No state income tax on lottery prizes (investment income only)

California is worth mentioning separately. It has one of the highest personal income tax rates in the country, but California specifically exempts lottery winnings from state income tax. A California winner pays federal taxes only. This is not intuitive and surprises many people who assume California would take a significant cut.

Alaska and Nevada have no state income tax, but neither state participates in Powerball or Mega Millions, so residents of those states would need to travel to play.

How Much Does It Actually Matter?

On a $500 million Powerball jackpot, the lump sum cash value is approximately $300 million before taxes. Here is how the after-tax take-home compares across different states after applying federal taxes at 37 percent:

- Florida (0%): approximately $189 million take-home

- Texas (0%): approximately $189 million take-home

- California (0% on lottery): approximately $189 million take-home

- Michigan (4.25%): approximately $176 million take-home

- Illinois (4.95%): approximately $174 million take-home

- Arizona (2.5%): approximately $182 million take-home

- Oregon (9.9%): approximately $159 million take-home

- Minnesota (9.85%): approximately $160 million take-home

- New Jersey (10.75%): approximately $157 million take-home

- New York (10.9%): approximately $156 million take-home

The difference between winning in Florida and winning in New York on this jackpot is approximately $33 million in state taxes. That is not a rounding error. It is a number that could fund multiple homes, businesses, or foundations.

The States With the Highest Lottery Taxes

On the opposite end of the spectrum, several states impose some of the highest tax rates on lottery prizes in the country:

- New York: 10.9%

- New Jersey: 10.75%

- Washington D.C.: 10.75%

- Oregon: 9.9%

- Minnesota: 9.85%

- Maryland: 8.75%

- Wisconsin: 7.65%

New York City adds another layer on top of the state rate. City residents pay a local income tax of up to 3.876 percent, which combines with the 10.9 percent state rate for a combined state and local burden approaching 15 percent. That makes New York City one of the most expensive places in the United States to win the lottery.

Can You Move Before Claiming to Avoid State Taxes?

This question comes up frequently, and the honest answer is that it is legally complicated and practically risky.

Your state of legal domicile at the time you claim the prize is generally what determines your state tax liability. Simply purchasing a ticket while visiting Florida does not make you a Florida resident for tax purposes if you live in Ohio. And attempting to rapidly establish residency in a no-tax state after winning but before claiming is something tax authorities in high-tax states are well aware of and may scrutinize aggressively.

Establishing genuine legal residency requires more than changing a mailing address. States look at where you spend the majority of your time, where your driver's license is issued, where you are registered to vote, and where your primary financial and social ties are. A winner who spends three weeks in Texas after a major jackpot win and then claims the prize as a Texas resident may face a challenge from their original home state.

If this is something you are considering, consult with a tax attorney who specializes in state residency issues before taking any action. Getting this wrong is expensive.

What About the State Where You Bought the Ticket?

In most cases, the state where you purchased the ticket does not determine your tax liability. You owe taxes to your state of residence. However, some states do withhold taxes at the source when a nonresident wins a prize above a certain threshold. If that happens, your home state typically gives you a credit for taxes paid to the other state to avoid double taxation.

The specific rules vary by state and prize size, and the interplay between source-state withholding and home-state tax credits can be complex. This is another area where having a qualified tax advisor in your corner pays for itself.

See Your State's Take-Home Estimate

Our calculator covers all 47 lottery jurisdictions, including all participating states, Washington D.C., and the U.S. Virgin Islands. Enter any jackpot amount and select your state to see an estimated after-tax take-home for both the lump sum and annuity options.

See Also

Ready to run the numbers?

Use our free calculator to see your estimated take-home amount.

Open Calculator